Tips for First-Time Home Buyers are an exciting and significant milestone. It is a journey filled with anticipation, planning, and crucial decisions. As a first-time home buyer, you might feel overwhelmed by the process, but understanding the steps involved can help you make informed choices and secure the home of your dreams. This guide will walk you through the essential aspects of buying your first home, from budgeting and mortgage options to finding the right property and navigating the closing process.

What is the First Step in Buying Your First Home?

This ratio helps lenders gauge your ability to manage monthly mortgage `payments alongside other debts. Once you’ve reviewed your financial status, begin saving for a down payment. While conventional wisdom suggests a 20% down payment, many first-time homebuyer programs offer loans with lower down payment requirements, sometimes as low as 3%.

How to Determine Your Budget for a First-Time Home Buyer?

Determining your budget is a critical step in the home buying process. Start by calculating your monthly income and expenses to see how much you can afford to allocate towards housing costs. Include all potential expenses such as principal, interest, property taxes, homeowner’s insurance, and possibly private mortgage insurance (PMI). Use the 28/36 rule as a guideline: your monthly mortgage payment should not exceed 28% of your gross monthly income, and your total debt payments (including the mortgage) should not exceed 36%.

using online tools like home affordability calculators to get a better understanding of what you can afford. These tools factor in your income, debt, and down payment to provide a realistic price range for your home search.

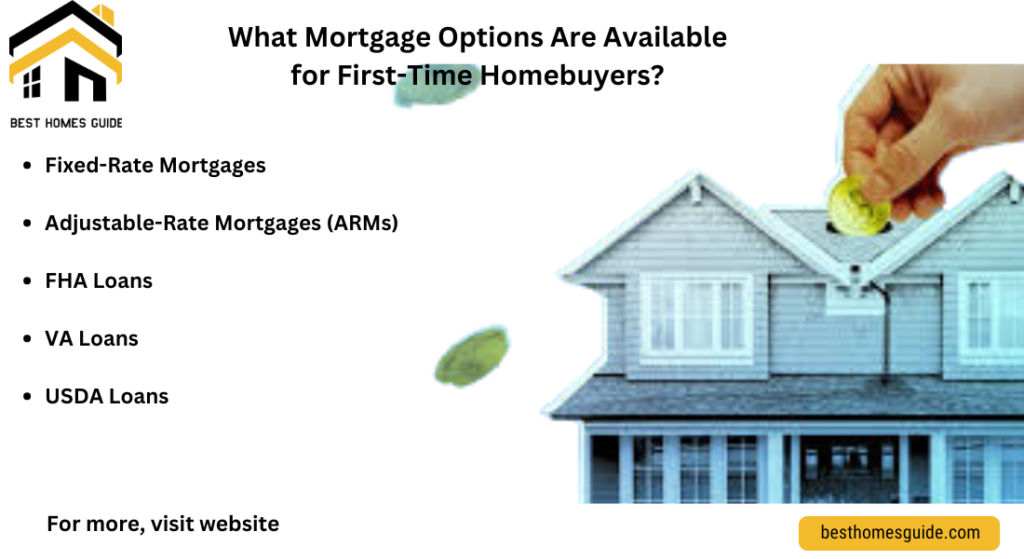

What Mortgage Options Are Available for First-Time Homebuyers?

First-time homebuyers have access to various mortgage options tailored to their needs:

- Conventional Loans: These are not backed by the government and typically require a higher credit score and a down payment of at least 5%, although some lenders may offer options as low as 3% for first-time buyers.

- FHA Loans: Insured by the Federal Housing Administration, FHA loans are popular among first-time buyers because they require lower down payments (as low as 3.5%) and have more lenient credit score requirements.

- VA Loans: Available to veterans and active-duty military personnel, VA loans offer benefits like zero down payment and no PMI. They are guaranteed by the Department of Veterans Affairs.

- USDA Loans: These are available for properties in designated rural areas and offer low interest rates with no down payment requirements, provided the borrower meets certain income criteria.

How to Get Pre-Approved for a Mortgage as a First-Time Buyer

Getting pre-approved for a mortgage is a crucial step for first-time homebuyers, as it provides a clear picture of your borrowing capacity and strengthens your position when making offers. To begin the process, gather essential financial documents such as proof of income, tax returns, and information on debts and assets. This documentation allows the lender to assess your creditworthiness and determine how much you can borrow.

A mortgage pre-approval involves submitting a loan application and undergoing a credit check. Unlike pre-qualification, which is a preliminary assessment based on self-reported data, pre-approval provides a more accurate borrowing limit as it is verified by financial documents. This process helps establish your credibility with sellers and real estate agents, indicating that you are a serious buyer capable of securing financing Finance smarter.

What Should You Look for in a Neighborhood and Location?

Choosing the right neighborhood and location is vital when buying your first home. Start by considering your lifestyle needs and priorities. Key factors include proximity to work, quality of local schools, access to public transportation, and availability of amenities such as shopping centers, parks, and recreational facilities. Safety is another crucial consideration; research local crime rates and talk to potential neighbors to get a feel for the area.

It’s also essential to look at the future development plans for the neighborhood. Areas with planned infrastructure improvements or commercial developments may offer better long-term value, And First-Time Home Buyer. They could also bring increased traffic and noise. Understanding these factors can help you choose a location that meets your current needs and offers good investment potential.

How to Find a Real Estate Agent for First-Time Buyers

Finding the right real estate agent is a key step in the First-Time Home Buyer, especially for first-time buyers. A good agent can provide valuable insights into the market, help you find properties that meet your criteria, and guide you through negotiations and the closing process. When selecting an agent, look for someone who is knowledgeable about the local market, responsive to your needs, and has experience working with first-time buyers.

Start by asking for recommendations from friends, family, or colleagues. You can also read reviews and check credentials online. It’s advisable to interview a few agents to find one who understands your needs and with whom you feel comfortable. A skilled agent can help you navigate the complexities of the market, from setting a realistic budget to making competitive offers.

What to Look for During Home Tours and Inspections?

When touring homes, it’s crucial to be thorough and attentive to detail. Start with structural and safety features, examining the foundation, walls, and roof for any signs of damage or potential issues. Look for cracks, water stains, or uneven floors, as these could indicate serious problems like foundational issues or water damage. Check the roof for missing shingles and the gutters for proper drainage. It’s also wise to test all windows and doors to ensure they open and close properly, which can indicate structural integrity and energy efficiency.

Inside the home, inspect the functionality of key systems and appliances. Turn on faucets and showers to check water pressure and temperature consistency. Test electrical outlets and light switches, and inquire about the age and condition of major appliances, such as the HVAC system, water heater, and kitchen appliances. Don’t forget to examine the attic and basement for insulation quality and any signs of moisture or pest infestations.

How to Make a Competitive Offer on a Home?

Making a competitive offer on a First-Time Home Buyer requires a strategic approach, especially in a hot market. Begin by understanding the market conditions—whether it’s a buyer’s or seller’s market can significantly influence your offer. In a seller’s market, you may need to offer above the asking price, while in a buyer’s market, you have more room for negotiation. Consider recent sales of similar homes in the area to gauge a reasonable offer price.

Strengthen your offer by being flexible with contingencies and closing terms. Sellers often favor offers with fewer contingencies because they reduce the chances of the deal falling through. Common contingencies include financing, home inspection, and appraisal. If possible, be flexible with the closing date to accommodate the seller’s timeline. A larger earnest money deposit can demonstrate your seriousness and financial stability, making your offer more attractive (Home Inspection Insider) (Atlantic Bay Mortgage).

What Are the Common Contingencies in a Home Purchase Contract?

Contingencies are conditions that must be met for a real estate transaction to proceed. The most common contingencies in a home purchase contract include the financing contingency, which protects the First-Time Home Buyer if they are unable to secure a mortgage loan. This is crucial as it allows the buyer to back out without penalty if financing falls through.

key contingency is First-Time Home Buyer the home inspection contingency, which allows the buyer to negotiate repairs or withdraw from the purchase based on the inspection results. This protects the buyer from unforeseen issues, such as structural defects or significant repairs needed. The appraisal contingency is also common; it ensures that the property’s value aligns with the purchase price, protecting the buyer and lender from overpaying.

How Does the Home Appraisal Process Work?

The home appraisal process is an essential step in the First-Time Home Buyer journey, especially for first-time buyers. It involves a licensed appraiser evaluating the property’s market value to ensure it aligns with the amount being financed by the mortgage lender. This process typically begins after the buyer and seller agree on a purchase price and sign a contract.

During the appraisal, the appraiser conducts a detailed inspection of the property, examining both the exterior and interior. Key factors assessed include the property’s condition, size, location, and any improvements or upgrades. The appraiser also considers comparable properties (comps) recently sold in the area to help determine the First-Time Home Buyer market value. This comparative analysis helps ensure that the lender is not lending more than the property’s worth, protecting both the lender and the buyer from overpaying.

What is the Importance of a Home Inspection for First-Time Buyers?

A First-Time Home Buyer inspection is a crucial step for first-time homebuyers, providing a detailed evaluation of the property’s condition. Unlike an appraisal, which focuses on determining market value, a home inspection identifies potential issues with the property’s structure and systems. This includes checking for problems with the roof, foundation, plumbing, electrical systems

What Are the Closing Costs and How to Budget for Them?

Closing costs are various fees and charges that homebuyers must pay to finalize a First-Time Home Buyer. They typically range from 2% to 6% of the loan amount. Common closing costs include lender fees, third-party fees, and prepaid expenses.

Lender Fees: These can include loan origination fees, application fees, and points paid to lower your interest rate. Lenders may charge for credit reports, flood determination, and the first year’s homeowners insurance premium.

Third-Party Fees: These fees cover services provided by third parties, such as the appraisal fee, home inspection fee, and title search and insurance. Title insurance protects the buyer and lender from potential legal issues with the property’s title. Other costs can include survey fees, attorney fees, and recording fees.

Prepaid Expenses: These are advance payments for property taxes and homeowners insurance, which are often placed in an escrow account. Prepaid interest, covering the interest due from the closing date until the first mortgage payment, is also included.

How Does the Closing Process Work?

The closing process, also known as settlement, is the final step in First-Time Home Buyer journey, where the ownership of the property is transferred from the seller to the buyer. This process involves several key steps:

- Reviewing the Closing Disclosure: This document, provided at least three business days before closing, details all the costs and fees associated with the transaction. It’s crucial to review it carefully to ensure accuracy and avoid unexpected costs.

- Final Walk-Through: Buyers typically conduct a final inspection of the property to ensure it is in the agreed-upon condition. This is the last chance to confirm that any negotiated repairs have been completed.

- Signing Documents: At the closing meeting, the buyer signs various legal documents, including the mortgage note and deed of trust, which outline the loan terms and give the lender a claim to the property if the loan is not repaid. The buyer also provides payment for the down payment and closing costs, often via certified check or wire transfer.

- Funding and Recording: The lender funds the loan, and the title company or attorney records the new deed and mortgage with the local government. This officially transfers ownership to the buyer, who then receives the keys to their new home.

What Should First-Time Homebuyers Expect After Closing?

After closing, there are several important steps and considerations for new homeowners:

- Mortgage Payments: Set up your mortgage payments, either through automatic payments or manual methods. Ensure you understand the payment schedule and amount due each month, including principal, interest, taxes, and insurance (often referred to as PITI).

- Homeownership Responsibilities: Begin to plan for regular home maintenance and unexpected repairs. Regular upkeep can prevent costly repairs and maintain the property’s value. Consider setting up a budget or savings fund for these expenses.

- Insurance and Taxes: Ensure that your homeowners insurance is up to date and that you understand your property tax obligations. Some homeowners choose to pay property taxes and insurance directly, while others may have these expenses included in their monthly mortgage payment through an escrow account.

- Community Involvement: Familiarize yourself with your new community and neighbors. Understanding local ordinances, joining homeowners associations (if applicable), and participating in community events can enhance your living experience.

How to Plan for the Ongoing Costs of Homeownership?

1. Budget for Maintenance and Repairs: Unlike renting, homeownership involves ongoing costs for maintenance and repairs. It’s essential to set aside funds for unexpected repairs, such as plumbing issues, roof repairs, or appliance replacements. A good rule of thumb is to save 1-3% of the First-Time Home Buyer value annually for maintenance.

2. Property Taxes and Insurance: Property taxes can vary significantly based on location and property value. Ensure you understand your tax obligations and consider them in your budget. Homeowners insurance is necessary to protect your investment. It’s crucial to review your policy annually to ensure adequate coverage, especially if you make significant improvements to your home.

3. Utility Costs and Homeowner Association (HOA) Fees: Homeowners are responsible for utilities like water, electricity, and gas. It’s essential to consider these costs when budgeting for homeownership. If your property is part of an HOA, you’ll also need to account for monthly or annual fees, which can cover amenities and maintenance of common areas (Investopedia) (Orchard Home Swap).

These steps can help first-time homebuyers avoid common pitfalls, take advantage of available financial assistance, and plan for the long-term costs of homeownership effectively.

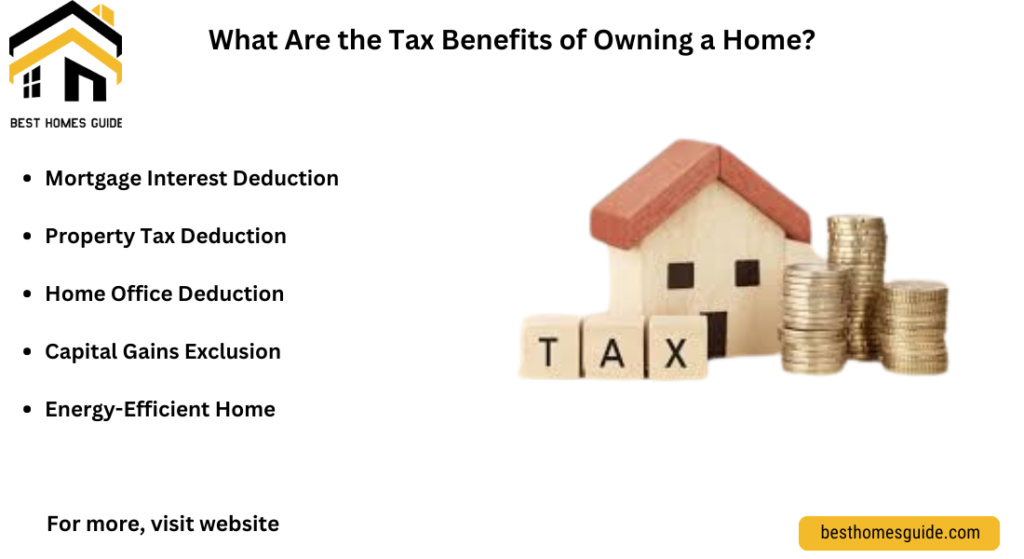

What Are the Tax Benefits of Owning a Home?

A home offers several tax benefits that can significantly reduce your annual tax burden:

- Mortgage Interest Deduction: Homeowners can deduct the interest paid on mortgages up to $750,000. This deduction is particularly beneficial for those who have recently purchased a home, as mortgage interest payments are often higher in the initial years of the loan.

- Property Tax Deduction: Homeowners can deduct up to $10,000 in property taxes, which includes state and local taxes, on their federal tax returns. This deduction helps reduce taxable income and, consequently, the overall tax bill.

- Mortgage Points Deduction: If you paid points to reduce your mortgage interest rate, these points are deductible. Typically, you can deduct the full amount of the points in the year they were paid, provided the loan is for your primary residence.

- Home Office Deduction: If part of your home is used exclusively for business, you may be eligible for a home office deduction. This can include a portion of utilities, mortgage interest, and other expenses .

How to Maintain and Improve Your Home Value Over Time?

Maintaining and improving your home value involves regular upkeep and strategic enhancements:

- Regular Maintenance: Routine tasks such as painting, cleaning gutters, servicing HVAC systems, and checking for leaks can prevent larger, more costly issues down the line. Regular maintenance not only preserves the condition of your home but also helps maintain its value.

- Home Improvements: Strategic upgrades can significantly enhance your home’s value. Key areas to focus on include kitchen and bathroom remodels, energy-efficient upgrades (like windows and insulation), and improving curb appeal through landscaping and exterior updates. These improvements often offer a high return on investment.

- Stay Informed on Market Trends: Understanding the local real estate market trends can guide your renovation and maintenance decisions. For example, if smart home technology or eco-friendly features are in demand, investing in these areas can make your home more attractive to future buyers.

- Documentation and Permits: Always document any improvements or repairs and ensure they comply with local building codes. This not only helps during the sale of your home but also ensures all work is legally recognized.

Advantage of these tax benefits and maintaining your property, you can maximize the financial advantages of homeownership and protect your investment over the long term.

How to Assess Financial Readiness and Secure Mortgage Pre-Approval for Buying Your First Home

Navigating the journey to homeownership as a first-time buyer can be both exciting and challenging. This guide has covered crucial aspects from understanding the initial steps, such as assessing financial readiness and securing a mortgage pre-approval, to selecting the right neighborhood and finding a reliable real estate agent. It emphasized the importance of thorough home inspections, making competitive offers, and understanding common contingencies in purchase contracts.

What Are the Key Steps in the Home Buying Process, from Choosing a Neighborhood to Closing?

The guide highlighted the significance of preparing for closing costs and the steps involved in the closing process, including the final walk-through and signing of documents. For new homeowners, being aware of ongoing responsibilities and potential financial assistance programs can ease the transition into homeownership. Understanding the tax benefits available, such as deductions for mortgage interest and property taxes, can offer significant financial relief.

The process of buying your First-Time Home Buyer requires careful planning, financial diligence, and a clear understanding of the responsibilities that come with homeownership. By avoiding common mistakes and taking advantage of available resources and tax benefits, first-time homebuyers , how to can make informed decisions and enjoy the many rewards of owning a home Finance smarter Orchard Home Swap, Finance.